Calculating usage involves determining the amount of usage of whatever activity measure is used to assign overhead costs, such as machine hours or direct labor hours used. Let’s continue our previous example and see how overheads will be absorbed using the overhead absorption rates that we’ve calculated previously. What we know from the first example is that the overhead absorption rate for department A was $20 per machine hour, and for department B it was $25 per labour hour.

Examples of fixed overhead costs include mortgage payments on factories, machine depreciation, and salaries for supervisors. Under absorption costing, the fixed manufacturing overhead costs are included in the cost of a product as an indirect cost. These costs are not directly traceable to a specific product but are incurred in the process of manufacturing the product. In addition to the fixed manufacturing overhead costs, absorption costing also includes the variable manufacturing costs in the cost of a product. These costs are directly traceable to a specific product and include direct materials, direct labor, and variable overhead.

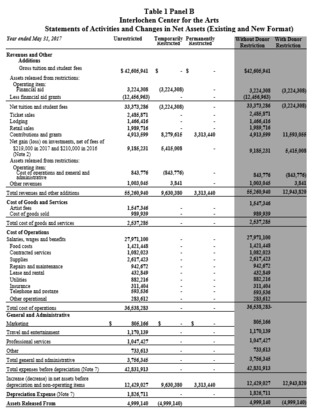

Step 1. Assign Costs to Cost Pools

The following is the step-by-step calculation and explanation of absorbed overhead in applying to Absorption Costing. Thus if the quantity of units produced exceeds the quantity of units sold, absorption costing will result in higher profit. (2) When units produced is greater than units sold, absorption costing yields the highest profit.

- What that budgeted level of activity is within the calculation of the overhead absorption rate, actually varies depending on the department under consideration.

- If you divide this by the number of units produced (say, 10), the cost per unit of production would be $60.

- Absorption costing includes all manufacturing costs, while other methods may only include direct costs.

Furthemore, it would allow us to set up budgets which are very, very important for the planning cycle of the business. Deciding which costing method to use for accrual accounting and prepayments product pricing is an important decision. It depends on factors such as the industry, market, product mix, competitive strategy, and accounting standards.

How to optimize your product pricing with absorption costing

Absorption costing means that ending inventory on the balance sheet is higher, while expenses on the income statement are lower. The labor cost involved in the production process includes the salaries or wages of permanent or contract workers. These are materials used in the production process, which includes the cost of purchasing each material. Absorption costing is a useful tool for decision-making and planning in a variety of contexts, as it helps a company understand the full cost of producing a product and how this cost relates to sales revenue.

This is because the fixed overhead is allocated based on the number of units produced, not on the number of units that actually use the overhead. This is because it includes all costs, regardless of whether they are variable or fixed. This means that the total cost of inventory may be higher than it should be, which can lead to incorrect pricing decisions. Both absorption costing and variable costing are methods used for inventory valuation and product costing. Both types of costing include direct materials, direct labor, and variable manufacturing overhead in their product cost calculations. The main difference is that absorption costing includes fixed-cost manufacturing overhead while variable costing does not.

Absorption Costing: Definition, Formula, Calculation, and Example

Additionally, it reduces the income volatility caused by changes in production volume and inventory levels, encouraging managers to increase production efficiency. Variable costing separates the fixed and variable costs, providing a clearer picture of the contribution margin of each product. It also aligns the income with sales volume, avoiding income inflation due to overproduction.

What is absorption costing with example?

Absorbed cost is an accounting method that includes both the direct costs and indirect costs involved in manufacturing goods. Absorbed costs can include expenses like energy costs, equipment rental costs, insurance, leases, and property taxes.

These costs include raw materials, labor, and any other direct expenses that are incurred in the production process. So, when we’re working out the overhead absorption rate for department B, we’re actually going to use the budgeted level of activity for labour hours, which is 4,000. Now, if you focus on department A, they’ve estimated budgeted labour hours of 2,000 and budgeted machine hours of 20,000. It means that the vast majority of the work done within this department is carried out by the equipment.

What Not to Include in an Absorption Costing System

These costs are also known as overhead expenses and include things like utilities, rent, and insurance. Indirect costs are typically allocated to products or services based on some measure of activity, such as the number of units produced or the number of direct labor hours required to produce the product. You need to consider direct material cost per unit, direct labor cost per unit, variable manufacturing overhead cost per unit, and fixed manufacturing overhead per unit. What that budgeted level of activity is within the calculation of the overhead absorption rate, actually varies depending on the department under consideration. Therefore, what we look for in questions if we need to determine this is whether or not a department is what we will call machine intensive or labour intensive.

What is an example of absorption company?

When one existing company takes over the business of one or more existing companies, it is absorption. The companies whose business is taken over are liquidated. No new company is formed. Real life example: hutch + Vodafone = Vodafone.